Something remarkable is happening in Ethiopia right now. A country where cash dominated almost every transaction just a few years ago is becoming one of Africa’s most interesting digital payment stories. Telebirr has grown into a platform serving tens of millions of users, CBE Birr has brought mobile money to customers of the country’s largest bank, and the National Bank of Ethiopia is actively pushing its national digital payments strategy to deepen usage and expand interoperability through 2029.

For entrepreneurs and businesses, this shift creates a once-in-a-generation opportunity. Whether you want to build a digital wallet, a lending platform, a savings app, or simply add payment functionality to your existing business app, the market conditions in 2026 are better than they have ever been. The catch is that fintech app development in Ethiopia comes with unique technical and regulatory requirements that generic app development guides never cover.

This guide fills that gap. We will walk through the fintech opportunity in Ethiopia, the types of apps worth building, how Telebirr and CBE Birr integration actually works, the security and compliance essentials you cannot skip, and what it all costs. If you are still at the stage of choosing a development partner, our guide to the top mobile app development companies in Addis Ababa pairs well with this one.

Why Ethiopia Is a Fintech Goldmine in 2026

Three forces are converging to make this moment special. First, infrastructure. Ethio Telecom’s expansion strategy aims to bring mobile broadband to the vast majority of the population, which means the addressable market for any mobile-first financial product grows every quarter. Second, policy. The National Bank of Ethiopia launched the second phase of its national digital payments strategy, focused on deepening usage, pushing interoperability between payment systems, and expanding digital ID integration. Regulators are actively encouraging the ecosystem rather than blocking it.

Third, and most importantly, user behavior has already changed. Millions of Ethiopians who never had a bank account now send money, pay bills, and buy airtime through their phones daily. Once people trust their phone with money, they are ready for the next layer of financial services: savings products, credit, insurance, investments, and merchant tools. That next layer is exactly where new fintech apps win.

The financial inclusion angle matters commercially too. A large share of the Ethiopian population remains underserved by traditional banking. Apps that serve these users well, in their language and within their data constraints, are not competing with established players. They are creating entirely new markets.

Types of Fintech Apps You Can Build in Ethiopia

- Digital wallets and payment apps. Apps that let users store value, transfer money, and pay merchants. These compete or partner with existing platforms and often differentiate through better UX or niche audiences.

- Digital lending platforms. Micro-loans and merchant credit scored through mobile money transaction history and alternative data. Credit access is one of the largest unmet needs in the Ethiopian market.

- Savings and equb apps. Digital versions of traditional Ethiopian rotating savings groups, with automated contributions, transparent records, and group management built in. This is a uniquely Ethiopian product opportunity with strong cultural fit.

- Merchant and agent tools. Point-of-sale apps, inventory plus payments combos, and agent banking apps that help small shops accept digital payments and track their business.

- Remittance apps. The Ethiopian diaspora sends substantial money home every year. Apps that make receiving international transfers cheaper and faster, with payout directly to Telebirr or bank accounts, address a massive existing flow.

- Payment-enabled business apps. Not every fintech app is a standalone financial product. E-commerce, delivery, transport, and booking apps all need payment integration, and doing it well is often what separates apps people use once from apps they use daily.

- Insurtech and investment apps. Earlier stage in Ethiopia, but micro-insurance and digital investment products are following the same adoption curve payments did. Early movers will define these categories.

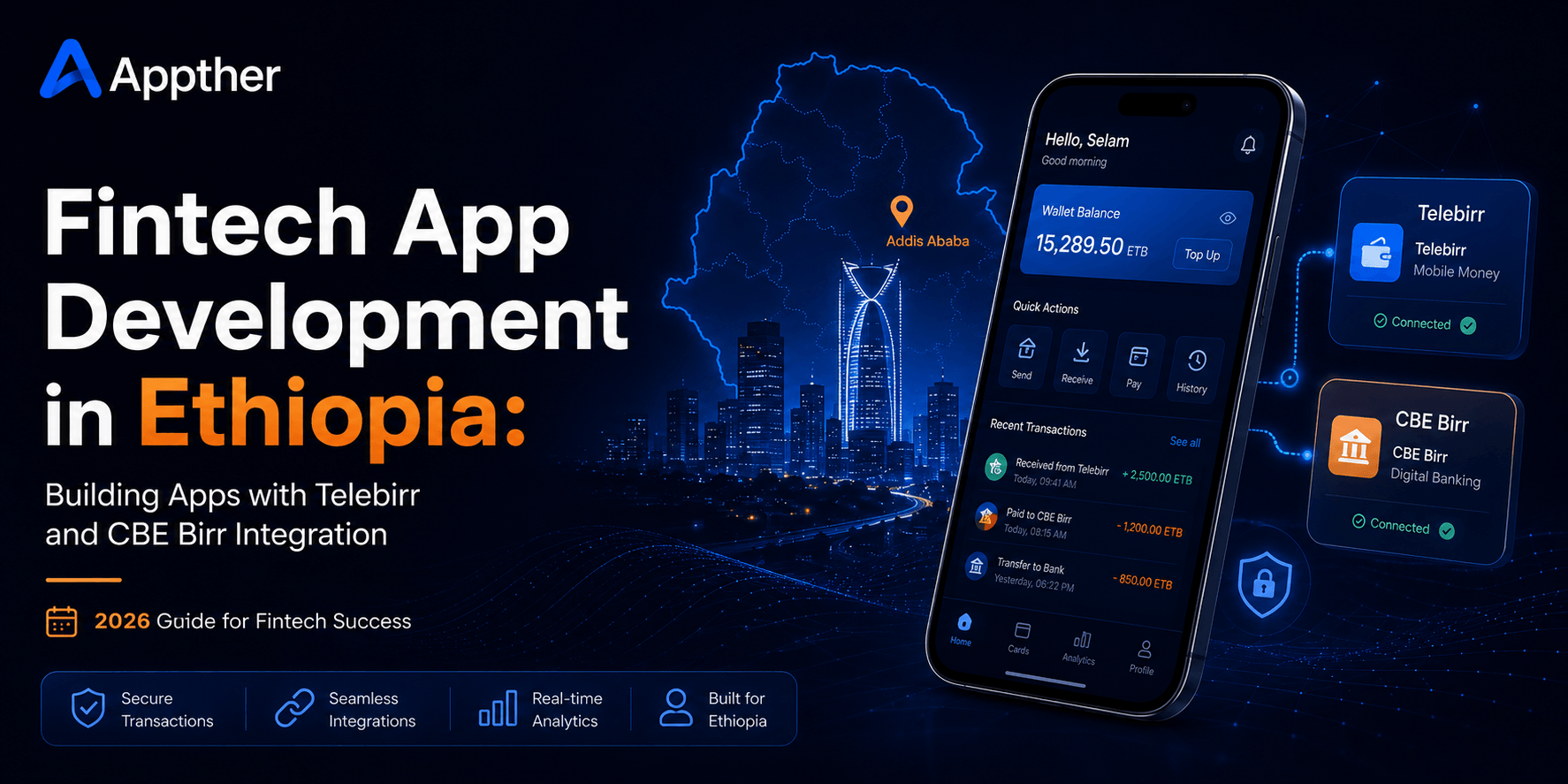

Telebirr Integration: How It Works

Telebirr is Ethio Telecom’s mobile money platform and the largest digital payment system in the country, which makes it the first integration almost every Ethiopian app needs. Telebirr offers integration options for businesses and developers that allow your app to accept payments from any Telebirr user.

The Typical Payment Flow

In a standard customer-to-business integration, the flow works like this. The user taps pay in your app, your backend creates a payment request through the Telebirr merchant integration, the user confirms the payment with their Telebirr PIN, and Telebirr notifies your backend that the transaction succeeded so your app can complete the order. The whole experience takes seconds when implemented well.

Beyond simple checkout, mature integrations also handle business-to-customer disbursements such as refunds, loan payouts, or seller settlements, plus reconciliation so your finance team can match every app transaction against the Telebirr statement automatically.

What Makes a Telebirr Integration Good Instead of Just Functional

- Robust failure handling. Mobile networks drop, users abandon payments halfway, and notifications occasionally arrive late. A good integration verifies transaction status with Telebirr rather than assuming, so users are never charged without receiving their order and never receive orders without paying.

- Idempotent transaction design. If the same payment confirmation arrives twice, your system must process it exactly once. This sounds obvious but is one of the most common defects in rushed integrations.

- Clear user communication. Pending, successful, and failed states should each look distinct in your app, in language your users actually understand, including Amharic where your audience expects it.

- Secure credential management. Merchant keys and API credentials belong in your secure backend, never inside the mobile app itself where they can be extracted.

CBE Birr Integration: Reaching Bank Customers

CBE Birr is the mobile money service of the Commercial Bank of Ethiopia, the country’s largest bank. For many users, especially those with existing CBE accounts and salary deposits, CBE Birr is their primary digital money channel. Supporting it alongside Telebirr meaningfully expands the share of Ethiopians who can pay inside your app.

The integration concepts mirror Telebirr: merchant onboarding with the bank, payment initiation from your backend, customer confirmation, and notification of the result. In practice, the commercial onboarding process with a bank takes longer than the technical work, so start the partnership conversation with CBE early, ideally while your app is still in development rather than after launch.

A practical architecture tip from real projects: build your payment layer as an abstraction rather than wiring Telebirr or CBE Birr directly into your business logic. With a payment gateway layer in your backend, adding the second provider, or a third one later as Ethiopia’s interoperability push matures, becomes a contained task instead of a rewrite. This is also how you future-proof for upcoming developments in the Ethiopian payments ecosystem, including the growing interoperability between wallets and banks driven by the national payment infrastructure.

Security and Compliance: The Non-Negotiables

Fintech apps carry responsibilities ordinary apps do not. When your app touches money, cutting corners on security is not a cost saving, it is an existential risk. These are the essentials every Ethiopian fintech app needs:

- Encryption everywhere. All data in transit must use TLS, and sensitive data at rest, including personal information and transaction records, must be encrypted in your database.

- Strong authentication. PIN or biometric login, plus a second factor for sensitive actions like adding a payout account or transferring above a threshold.

- KYC workflows. Know Your Customer verification is a regulatory requirement for financial services. Ethiopia’s expanding digital ID program (Fayda) is increasingly relevant here, and designing your onboarding to work with national ID verification positions you well for where regulation is heading.

- Fraud monitoring. Velocity checks, unusual pattern detection, and transaction limits protect both your users and your business. AI-based fraud detection is becoming standard in serious fintech products.

- Regulatory alignment with the NBE. Depending on what your app does, you may need to operate under a payment instrument issuer license, partner with a licensed institution, or register appropriately. Get legal advice early, because the right licensing path shapes your product architecture. Many successful apps launch faster by partnering with an existing licensed bank or payment provider rather than pursuing their own license first.

- Audit trails. Every transaction, status change, and administrative action should be logged immutably. Regulators expect it, and you will thank yourself the first time you investigate a disputed transaction.

Designing for Ethiopian Users

Technical integration is only half the work. Fintech apps succeed in Ethiopia when they respect how Ethiopian users actually live and transact. That means Amharic language support done properly, not as an afterthought, and ideally additional local languages depending on your target regions. It means lightweight apps that perform well on affordable Android devices and tolerate unstable connectivity, with clear offline states instead of endless spinners. And it means building trust deliberately, with transparent fees, instant transaction confirmations by SMS or push notification, and responsive customer support.

On that last point, AI is changing what is possible for customer support in the Ethiopian market. Banks and fintechs are deploying AI-powered chatbots that handle customer service in Amharic around the clock, answering balance questions, guiding users through failed transactions, and escalating only the genuinely complex cases to human agents. For a fintech app, embedding this kind of assistant directly in the product reduces support costs dramatically while improving the trust that drives retention.

What Does Fintech App Development Cost in Ethiopia?

Fintech apps cost more than ordinary apps because of security, compliance, and integration requirements. In 2026, a payment-enabled business app typically starts around $15,000 to $25,000, a focused fintech MVP such as a wallet or lending product generally runs $20,000 to $50,000, and full-scale platforms with multiple financial products go well beyond that. Telebirr or CBE Birr integration alone typically adds $1,500 to $5,000 depending on the complexity of your transaction flows. For a complete breakdown of pricing by app type, development stage, and the hidden costs to budget for, see our detailed mobile app development cost guide for Ethiopia.

The smartest way to manage fintech budgets is the MVP approach. Launch with one core financial function done excellently, prove the model with real users and real money, then expand. Trying to launch a super-app on day one multiplies cost, regulatory complexity, and risk simultaneously.

How to Choose a Fintech Development Partner

Fintech is the one category where partner selection matters most, because mistakes are expensive and visible. Beyond the usual portfolio review, ask any shortlisted agency these questions. Have you integrated Telebirr or CBE Birr in a live production app, and can we see it? How do you handle failed and duplicate transactions? What is your approach to KYC and NBE compliance? How do you secure credentials and sensitive data? What does your post-launch monitoring and support look like? Vague answers to any of these are disqualifying.

Appther brings exactly this combination to Ethiopian fintech projects. The team has delivered 500+ projects across 40+ countries, builds with modern cross-platform frameworks like Flutter and React Native for fast Android and iOS coverage, and pairs mobile app development with in-house AI engineering for fraud detection, intelligent chatbots, and analytics. Security and compliance are built into the process from the first architecture diagram, with NDA protection and full IP transfer as standard practice.

Frequently Asked Questions

Can any app integrate Telebirr payments?

Yes, provided your business completes Telebirr’s merchant onboarding requirements with Ethio Telecom. Once approved, your development team can integrate the payment flows into your app. The technical work typically takes a few weeks; allow additional time for the commercial onboarding process.

Should I integrate Telebirr or CBE Birr first?

For most consumer apps, Telebirr first, because of its larger user base, then CBE Birr to capture bank-first customers. If your audience skews toward salaried CBE account holders, the order may reverse. Building your payment layer as an abstraction makes adding the second provider straightforward either way.

Do I need a license from the National Bank of Ethiopia?

It depends on your model. Simply accepting payments for your own goods and services through licensed providers generally does not require your own license. Holding customer funds, issuing wallets, or lending typically does, or requires partnering with a licensed institution. Consult an Ethiopian fintech lawyer before finalizing your product scope.

How long does it take to build a fintech app?

A focused fintech MVP typically takes 4 to 6 months including payment integration, security hardening, and testing. Allow extra time for merchant onboarding with payment providers and any licensing or partnership processes, which can run in parallel with development if planned early.

Can AI features really help a fintech app?

Significantly. The highest-impact applications are fraud detection, Amharic customer support chatbots, credit scoring from alternative data, and personalized financial insights for users. These features increasingly separate market-leading fintech products from commodity ones.

Final Thoughts: The Window Is Open Now

Ethiopia’s fintech story is still in its early chapters. The infrastructure is arriving, the regulator is engaged, and tens of millions of users have already made the leap to mobile money. The companies that build well-engineered, locally-attuned financial products in the next two to three years will own categories that barely exist today.

If you have a fintech idea for the Ethiopian market, the best next step is a conversation with a team that has done this before. Book a free consultation with Appther to discuss your concept, get honest guidance on scope, compliance, and budget, and receive a clear milestone-based roadmap from idea to launch. The opportunity is real, and with the right partner, so is your app.